Este blog ha terminado, pero permanecerá en línea. Hemos comenzado un nuevo blog, Carpeta Monetaria, en donde Genevieve Signoret está en la conversación global sobre política monetaria.

Gracias por su lectura y sus comentarios. ¡Esperamos verlos en Carpeta Monetaria!

22 June 2011

17 November 2010

What Roubini said / Lo que dijo Roubini

(Para español, desplácese hacia abajo.)

Nouriel Roubini made various claims and predictions today in an interview on CNBC:

Hoy en entrevista en CNBC, Nouriel Roubini predijo y afirmó:

Nouriel Roubini made various claims and predictions today in an interview on CNBC:

- QE2 will be followed by several more rounds, up to QE4 or QE5. (This prediction matches the TransEconomics view that, if necessary, the Fed will end up more than doubling the size of its balance sheet to to $5 trillion.)

- David Cameron and Mervyn King in the UK have an implicit agreement whereby the Bank of England will offset Treasury tightening with monetary loosening. The monetary loosening will take the form of QE2 a l'anglaise and will start as soon as fiscal pain (rock throwing) becomes unbearably intense.

- Given falling output in the European Union periphery and deflationary fiscal policy in Europe, the European Central Bank's current resistance to more quantitative easing is "not productive".

- We will probably see private orderly restructuring of sovereign debt in Greece first, then Portugal, and finally Ireland.

- Restructuring can take the form of exchange deals: sovereigns exchange outstanding bonds for some other assets. This is worked out with bondholders: no supranational entity (EU or IMF) need be involved.

- QE2 in the USA coupled with insufficiently fast appreciation of the Chinese yuan can lead to new or enlarged existing asset bubbles in China, even if China tightens credit and money.

Hoy en entrevista en CNBC, Nouriel Roubini predijo y afirmó:

- Después de esta ronda de estímulo cuantitativo (QE2) nos esperan más rondas, hasta QE4 or QE5. (Este punto es consistente con nuestra opinión en TransEconomics de que, si es neceario, la Fed más que duplicará el tamaño de su balance, hasta $5 billones.)

- David Cameron y Mervyn King en el Reino Unido tienen un acuerdo implícito según el cual Banco de Inglaterra contrarrrestará la política restrictiva del Tesoro con estímulo cuantitativo. El estímulo tomará la forma de un QE2 a la inglesa y comenzará tan pronto el dolor fiscal se torne insportable (los disturbios aumenten).

- Dada la contracción económica en la periferia de la Zona del Euro y la restricción fiscal en Europa, la resistencia del BCE a aplicar más estímulo cuantitativo (que el BCE llama "relajamiento crediticio") "no es productiva".

- Probablemente veremos una ordenada reestructuración privada de deuda en Grecia, primero, luego Portugal e Irlanda.

- Estos soberanos pueden canjear bonos por algún otro activo. El trato puede hacerse con inversionistas privados, sin que intervenga ninguna institución subpranacional del tipo FMI o Unión Europea.

- Aunque China restrinja el crédito y el dinero, QE2 en EEUU y demasiado lenta depreciación del yuan pueden provocar que en China la inflación se acelere y las burbujas financieras se multipliquen y se expandan.

08 November 2010

Fed lending standards, Fed Bullard speech, OECD leading indicator

Here are links to this morning's key global releases:

Fed: The October 2010 Senior Loan Officer Opinion Survey on Bank Lending Practices. Key quote (bold face is mine):

When nominal rates are at zero, as they are today, the Fed needs to persuade the public that in the future inflation will accelerate and stay rather high. (Which is not to say that hyperinflation will set in. Hyperinflation is of cours undesirable, but more importantly, it's in no way an inevitable consequence of QE, in my view. I don't even see it as a threat.)

OECD Composite Leading Indicators. Key content:

Fed: The October 2010 Senior Loan Officer Opinion Survey on Bank Lending Practices. Key quote (bold face is mine):

The October survey indicated that, on net, banks eased standards and terms over the previous three months on some categories of loans to households and businesses.2 Both large and other domestic banks reported having eased some standards and terms; large banks were primarily responsible for the easing reported in July.3 However, substantial fractions of banks reported in response to a set of special questions that standards for many categories of loans would not return to their longer-run averages for the foreseeable future.SF Fed Bullard's speech. Highlight:

Bullard said the FOMC must defend its implicit inflation target from the low side as it would from the high side. Since U.S. short-term interest rates are already approximately zero, further disinflation would mean rising real interest rates in the face of a slowing pace of recovery.Remember that we economists believe that people make saving and investment decisions based on the real interest rate: the nominal rate minus the rate of inflation expected over the investment decision time horizon.

When nominal rates are at zero, as they are today, the Fed needs to persuade the public that in the future inflation will accelerate and stay rather high. (Which is not to say that hyperinflation will set in. Hyperinflation is of cours undesirable, but more importantly, it's in no way an inevitable consequence of QE, in my view. I don't even see it as a threat.)

OECD Composite Leading Indicators. Key content:

OECD composite leading indicators (CLIs) for September 2010 point to diverging patterns of economic growth across major economies.

The CLIs show signs of continuing expansion in Germany, Japan, the United States and Russia, while pointing to a moderate downturn in Canada, France, India, Italy and the United Kingdom.

The CLIs for Brazil and China continue to point strongly downwards, edging below the long term trend and implying that the level of industrial production will fall below its longer-term trend in these two economies.

There's no time to get this into Spanish, now, as I'm heading out the door on a business trip.

Follow me on Twitter: @gisgnoret

Zoellick, explain yourself. Zoellick, explíquese.

Zoellick wrote this:

Martin Wolf argued (persuasively, in my view) against a gold standard last week.

Gold prices move up and down with global levels of fear. We're to link exchange rates to fear? Even when we might fear opposite things (deflation, inflation)?

*****

Zoellick escribió esto (es mi traducción):

Martin Wolf arguyó en contra de un estándar de oro (en mi opinión de manera persuasiva) la semana pasada.

El precio del oro sube y baja con el nivel global de miedo. ¿Debemos vincular la política cambiaria al miedo? ¿Aunque temamos fenómenos contradictorios (deflación, inflación)?

The [G20] system should also consider employing gold as an international reference point of market expectations about inflation, deflation and future currency values.Krugman and De Long have already responded (impolitely).

Martin Wolf argued (persuasively, in my view) against a gold standard last week.

Gold prices move up and down with global levels of fear. We're to link exchange rates to fear? Even when we might fear opposite things (deflation, inflation)?

*****

Zoellick escribió esto (es mi traducción):

El sistema [G20] debería también contemplar el uso del oro como referencia internacional de las expectativas en torno a la inflación, la deflación y cuánto valdrá en el futuro cada divisa.Krugman y De Long ya contestaron (de manera descortés).

Martin Wolf arguyó en contra de un estándar de oro (en mi opinión de manera persuasiva) la semana pasada.

El precio del oro sube y baja con el nivel global de miedo. ¿Debemos vincular la política cambiaria al miedo? ¿Aunque temamos fenómenos contradictorios (deflación, inflación)?

06 November 2010

Hoy sí

Bernanke explicó QE2 para el público en el Washington Post el jueves pasado. El párrafo clave es el siguiente:

Pero con una excepción: antes no se justificaban decisiones de política monetaria por su efecto en los precios accionarios.

Hoy sí.

This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.Justifca otra ronda de relajamiento cuantitativa (quantitative easing, or QE) con base en lo siguiente:

- Funcionó en el pasado (en la primera ronda).

- Con sólo anunciar la intención avanzó la bolsa de valores.

- Promoverá crecimiento económico: bajando las tasas de interés hipotecarias; bajando los rendimientos de los bonos corporativos (lo que promoverá inversión fija); elevando los precios accionarios, lo que, por enriquecer a los consumidores, puede impulsar más gasto.

Pero con una excepción: antes no se justificaban decisiones de política monetaria por su efecto en los precios accionarios.

Hoy sí.

Sígueme en Twitter: @gsignoret

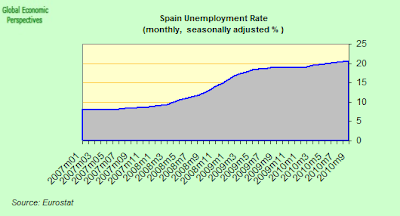

I'm glad we use Eurostat for Spanish labor data

Edward Hughes warns us to be careful in interpreting Spanish labor data. It's a good lesson in the perils of trying to perceive changes on the margin from data not seasonally adjusted. Hughes is scathing in tone:

But the way they present the data isn’t interesting, in fact its downright misleading. In particular they chose not to seasonally adjust the data – which in a seasonally driven economy like the Spanish one with significant ups and downs in tourist activity doesn’t make much sense – and this omission is not only lazy, it is negligent. (Read the whole post.)It turns out that although Spain's statistical agency's (INE's) unadjusted unemployment series shows month-on-month improvement, the seasonally adjusted series shows worsening.

For our own global macro database we have always relied on Eurostat's time series for Spain. We did this for one-stop shopping and comparability with the rest of the Euro Area.

Now we have another justification.

How might QE2 boost commodities prices? ¿Cómo podría QE2 elevar los precios de las materias primas?

(Para la versión en español, desplácese hacia abajo.)

The Fed's second round of quantitative easing (QE2) can boost commodities prices through four channels. First, by depressing Treasury yields in the middle of the yield curve and (it is hoped) by inflating prices generally, it can exert downward pressure on the U.S. dollar against other currencies such as the euro.

Of course, this would boost global commodities prices in dollar terms only (it would have the opposite effect on prices in euro terms, for example).

This tranmission channel pertains to all segments of commodities. Equally, it pertains to all other traded goods and services priced in U.S. dollars. QE2 is aimed, after all, at inflating dollar prices.

Second, by generating confidence that the U.S. economy will avert deflation and thus stir up hopes that growth will take off, it can draw speculators into the futures markets for industrial commodities: energy commodities and base metals.

Third, by generating fear of hyperinflation even while boosting high hopes for industrial commodities (in an unusual confluence of events), it can provide support for precious metals. Of course, this support will be iffy and unstable, as with any price support that relies on mere raw feelings such as fear.

Fourth, by depressing Treasury yields (in the middle of the curve), it can draw investors desperate for yield into the asset class.

**************

La segunda ronda de relajamiento cuantitativo (QE2) de la Fed puede dar ímpetu a los precios de las materias primas por cuatro vías. Primero, al deprimir los rendmientos de los bonos del Tesoro en medio de la curva, puede deprimir el dólar frente a otras monedas como es el euro.

Claro, este fenómeno reforzaría los precios de las materias primas en términos únicamente del dólar (tendría el efecto contrario en las cotizaciones en euros, por ejemplo).

Esta via se aplicaría a todos los segmentos de las materias primas. Asímismo, se aplicaría a la cotización en dólares de cualquier otro bien o servicio transable. El propósito del QE2, recuérdese, es inflar los precios en dólares.

Segundo, si genera confianza en que la economía estadounidense puede evitar la deflación y así despertar esperanzas de que el crecimientos despegue, puede atraer inversión especulativa hacia los mercados de futuros de materias primas industriales: energéticos y metales base.

Tercero, al generar miedo de hiperinflación al mismo tiempo que despertar esperanzas para las materias primas industriales (en una coincidencia de eventos inusitada), puede dar soporte a los metales preciosos. Claro, dicho soporte será incierto e inestable, como suele ser el caso cuando un precio toma su soporte de puros sentimientos primitivos.

Cuarto, al deprimir los rendimientos del Tesoro (a la mitad de la curva), puede incitar a inversionistas en búsqueda desesperada de retornos a entrar en esta categoría de inversión.

The Fed's second round of quantitative easing (QE2) can boost commodities prices through four channels. First, by depressing Treasury yields in the middle of the yield curve and (it is hoped) by inflating prices generally, it can exert downward pressure on the U.S. dollar against other currencies such as the euro.

Of course, this would boost global commodities prices in dollar terms only (it would have the opposite effect on prices in euro terms, for example).

This tranmission channel pertains to all segments of commodities. Equally, it pertains to all other traded goods and services priced in U.S. dollars. QE2 is aimed, after all, at inflating dollar prices.

Second, by generating confidence that the U.S. economy will avert deflation and thus stir up hopes that growth will take off, it can draw speculators into the futures markets for industrial commodities: energy commodities and base metals.

Third, by generating fear of hyperinflation even while boosting high hopes for industrial commodities (in an unusual confluence of events), it can provide support for precious metals. Of course, this support will be iffy and unstable, as with any price support that relies on mere raw feelings such as fear.

Fourth, by depressing Treasury yields (in the middle of the curve), it can draw investors desperate for yield into the asset class.

Follow me on Twitter: @gsignoret

**************

La segunda ronda de relajamiento cuantitativo (QE2) de la Fed puede dar ímpetu a los precios de las materias primas por cuatro vías. Primero, al deprimir los rendmientos de los bonos del Tesoro en medio de la curva, puede deprimir el dólar frente a otras monedas como es el euro.

Claro, este fenómeno reforzaría los precios de las materias primas en términos únicamente del dólar (tendría el efecto contrario en las cotizaciones en euros, por ejemplo).

Esta via se aplicaría a todos los segmentos de las materias primas. Asímismo, se aplicaría a la cotización en dólares de cualquier otro bien o servicio transable. El propósito del QE2, recuérdese, es inflar los precios en dólares.

Segundo, si genera confianza en que la economía estadounidense puede evitar la deflación y así despertar esperanzas de que el crecimientos despegue, puede atraer inversión especulativa hacia los mercados de futuros de materias primas industriales: energéticos y metales base.

Tercero, al generar miedo de hiperinflación al mismo tiempo que despertar esperanzas para las materias primas industriales (en una coincidencia de eventos inusitada), puede dar soporte a los metales preciosos. Claro, dicho soporte será incierto e inestable, como suele ser el caso cuando un precio toma su soporte de puros sentimientos primitivos.

Cuarto, al deprimir los rendimientos del Tesoro (a la mitad de la curva), puede incitar a inversionistas en búsqueda desesperada de retornos a entrar en esta categoría de inversión.

Sígame en Twitter: @gsignoret

Subscribe to:

Posts (Atom)